What Does a Data Breach Mean for You and Your Customers?

Every second, 60 data records – many of which contain private customer information – are compromised in a data breach.i In the last four years, over 9 trillion data records have been lost or stolen,ii putting everyone’s information at risk. The frequency and breadth of data breaches pose a very serious threat to your customers, enabling hackers to move money, make fraudulent purchases, and ruin credit scores. For financial institutions, which are often the target of fraudsters armed with stolen records, the scope of the damage can be extreme, as customers lose faith in banks that have been breached or where they have been defrauded. In addition to losing customers and reputation, financial institutions face serious financial repercussions from regulators, reimbursing customers, and defending against class action lawsuits. Regardless of where a data breach occurs, from large retailers to credit card companies or massive government databases, individuals and financial institutions often bear the brunt of the damages.

The devastating effects of a data breach for victimized individuals

When a data breach occurs, personal information is exposed, representing a significant breach of privacy. Unfortunately, the breach of privacy is only the beginning—hackers buy and sell stolen records on the dark web, and fraudsters quickly start leveraging personal information for financial gain. Innocent people lose money, at an average rate of $221 for each stolen record.iii Additionally, accounts or cards opened in an unsuspecting victim’s name can wreck their credit score—impacting their ability to buy a house, rent an apartment, buy a car, or change jobs.

Fixing a credit history damaged by fraud can be a costly, difficult, and time-consuming process for the victim.

If fraudsters don’t get all the information they need from a data breach, they may target individuals with further hacking or social engineering to get more information. Fraudsters use emails (phishing), phone calls (vishing), or text messages (smishing) to get individuals to provide additional personal information. Once they’ve got all the personal information they need, fraudsters can target financial institutions—where they can open new credit cards, withdraw money, and wreak havoc on an individual’s financial record.

Data breaches damage financial institutions’ profits, reputation, and customer experience

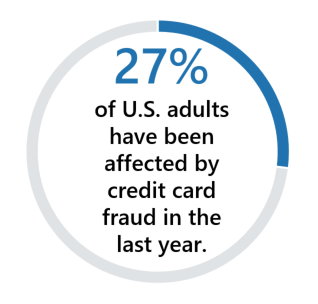

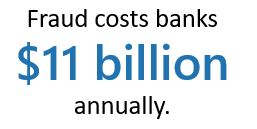

In addition to affecting individuals, data breaches also cause financial institutions to lose money and suffer reputational damage and potential regulatory action. Even if the data breach does not occur at a financial institution, they still often face the consequences. Between the actual fraud and the response to it, fraud costs financial institutions approximately $11 billion annually.iv Additionally, as 22 percent of fraud victims close at least one bank account,v financial institutions must spend resources creating new accounts for victims and may lose customers who decide to move to another bank. One of the most common types of data breaches involves credit card information being stolen, with 27 percent of U.S. adults having been affected by stolen credit card information in the last year.vi

In addition to affecting individuals, data breaches also cause financial institutions to lose money and suffer reputational damage and potential regulatory action. Even if the data breach does not occur at a financial institution, they still often face the consequences. Between the actual fraud and the response to it, fraud costs financial institutions approximately $11 billion annually.iv Additionally, as 22 percent of fraud victims close at least one bank account,v financial institutions must spend resources creating new accounts for victims and may lose customers who decide to move to another bank. One of the most common types of data breaches involves credit card information being stolen, with 27 percent of U.S. adults having been affected by stolen credit card information in the last year.vi

Exploiting the weaknesses in traditional security after a credit card breach

The lifecycle of a credit card breach demonstrates the devastating impacts a data breach has on individuals and financial institutions while providing useful insight into the weaknesses of standard digital security systems. As consumers try to deal with the aftermath of stolen cards or new ones issued in their names, they lose time and money, and their credit scores often take a hit. Card-issuing companies, meanwhile, spend significant resources investigating fraud, fraud detection, monitoring hacker channels, advising card holders, and implementing new rules. Even so, customers may still change their spending habits by closing accounts and tossing their credit and debit cards, ultimately damaging the financial institution’s bottom line.

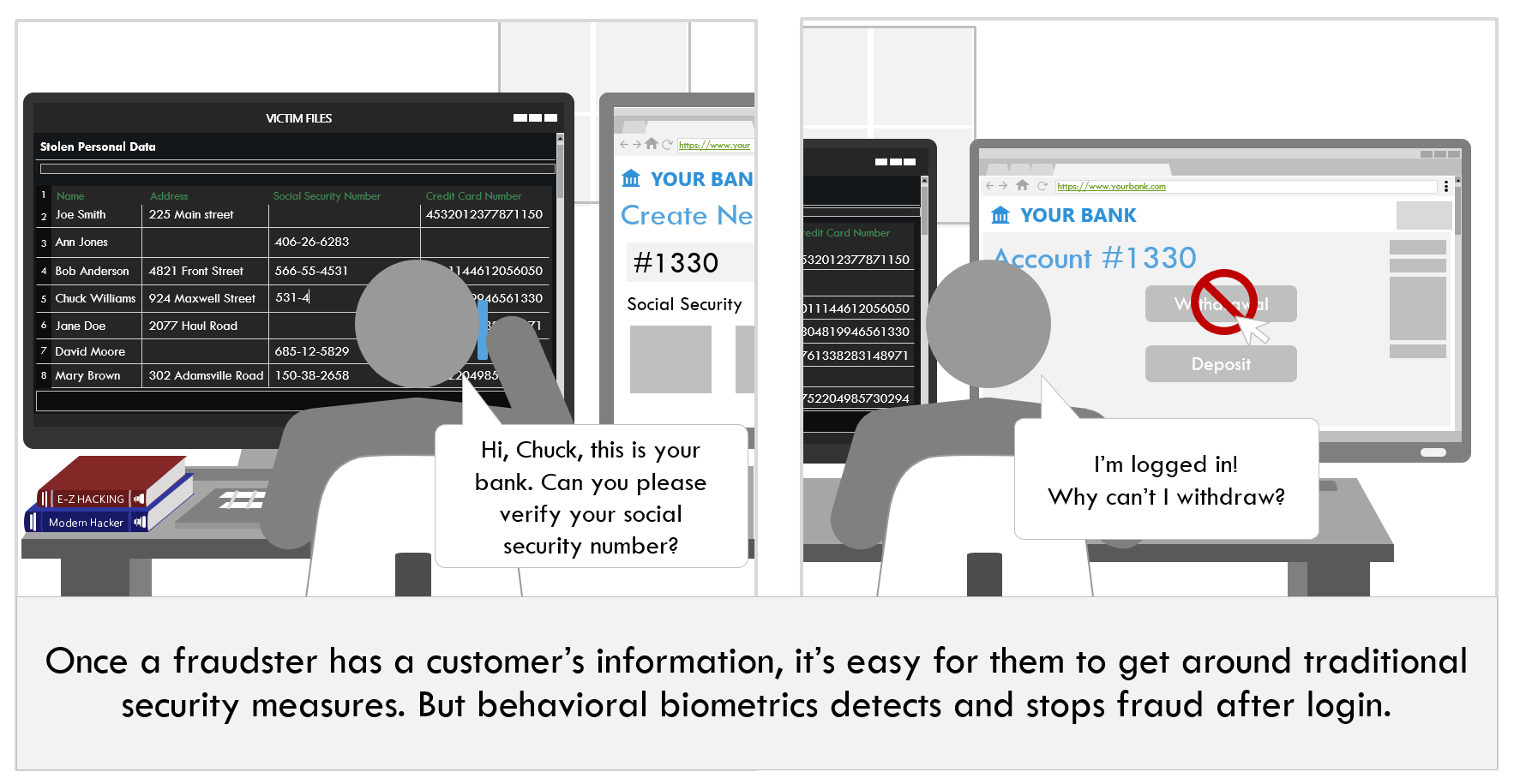

So how do financial institutions protect themselves from data breaches—even when they occur at a retailer or other business? Behavioral biometric security can hold the key, by looking at how information is entered, not what information is entered. For example, while a carder may be able to collect personal information, they cannot effectively copy or steal the way an individual interacts with their device(s) or enters information into an online form.

Transform security and protect against data breaches with a new solution

You can’t prevent all data breaches from occurring, but you can stop fraudsters from using stolen information at your financial institution. BioCatch, built on Microsoft Cloud technology, offers a behavioral biometric security solution that verifies a user’s identity with approximately 2,000 parameters, such as how a user scrolls, swipes, holds their device, and more.

Every month, BioCatch monitors over 5 billion transactions for 50 million users, saving banks millions of dollars annually by reducing fraud. Leveraging BioCatch, one leading U.K. bank demonstrated a fraud detection rate of 95 percent with less than 1 percent false positives. Learn more about how BioCatch will pay dividends in terms of consumer trust, reduced fraud, and more, by trying the solution on Microsoft AppSource today.

Visit Microsoft AppSource and try the solution today.

[i] Breach Level Index, http://breachlevelindex.com/, 2017

[ii] Breach Level Index, http://breachlevelindex.com/, 2017

[iii] Ponemon, 2016

[iv] Forbes, 2011, https://www.forbes.com/sites/haydnshaughnessy/2011/03/24/solving-the-190-billion-annual-fraud-scam-more-on-jumio/#586b6e24390e

[v] ACI Worldwide and Aite Group Survey: fi.deluxe.com/community-blog/fraud-id-theft/rebuilding-bank-customer-trust-fraud/

[vi] http://news.gallup.com/poll/196802/americans-credit-card-information-getting-hacked.aspx