Preventing the pain of transaction screening in banking

The 24-hour news cycle can make it feel like crime and terrorism are a near-constant in today’s world. The funding for these activities often stems from sanction-defying transactions. These transactions pass through banks that lack the ability or the motivation to accurately screen for illicit transactions. Increasingly, governments are attempting to crack down on these payments – so lawmakers have been escalating pressure on banks to stop dangerous or sanctioned transactions that contribute to global crime.

Today, executives are now personally liable for any illicit transactions that slip through. Noncompliance to strict regulations can cost banks dearly – fines related to sanctions have cost US banks over $200 billion between 2008 and 2015.[i] In order to prevent crime and protect themselves from fines, banks need rigorous sanction-screening solution that will solve the following three pain points:

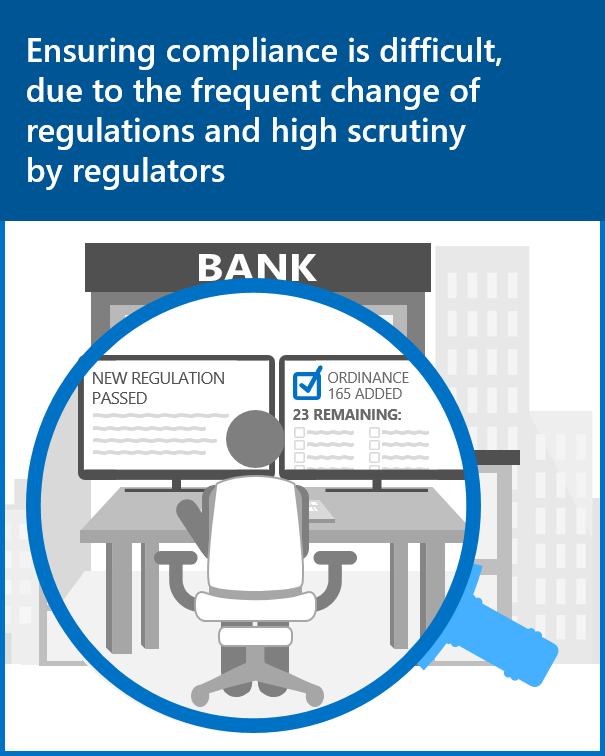

- Ensuring compliance is difficult, due to the frequent change of regulations and high scrutiny by regulators

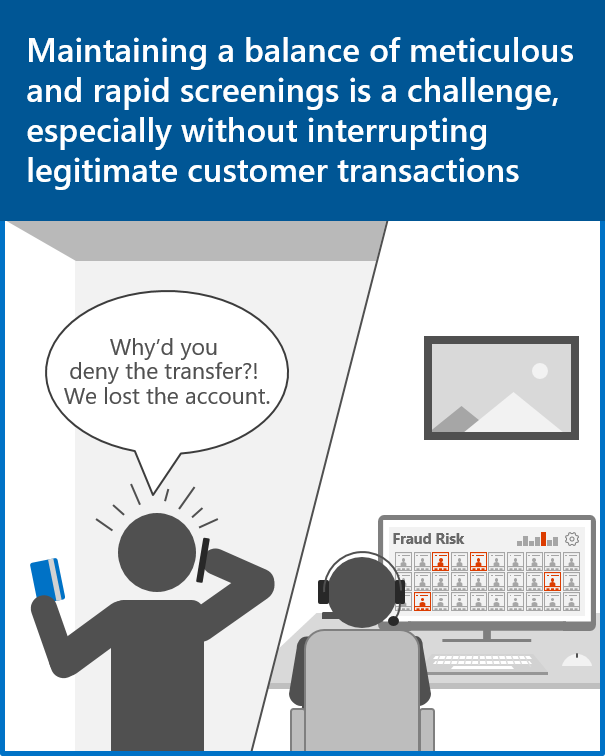

- Maintaining a balance of meticulous and rapid screenings is a challenge, especially without interrupting legitimate customer transactions

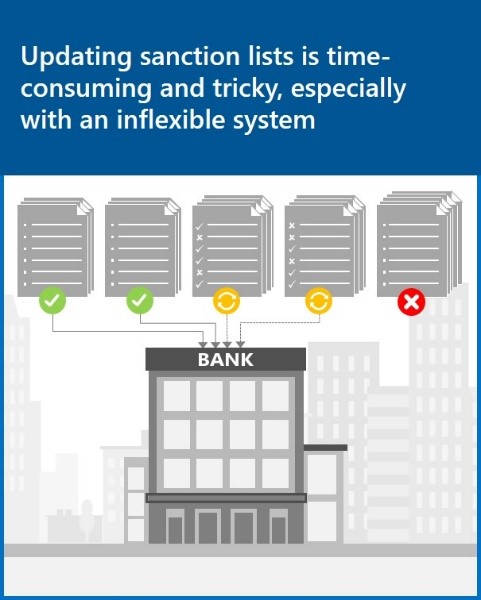

- Updating sanction lists is time-consuming and tricky, especially with an inflexible system

1. Ensuring compliance is difficult

Intense regulatory scrutiny in response to terror funding and other sanctioned transactions has created immense challenges for banks. 20% of financial services have experienced enforcement actions by a regulator, and that number is likely to grow.[ii] Banks face massive fines, operational shutdowns and reputational risk, if they don’t check against regulations and ensure all informational gaps are filled before a transaction occurs. And banks are not the only ones that suffer if they do not comply – their customers are experiencing an impact from the compliance crackdown as well. A bank in Asia was ordered by regulators to completely cease operations due serious regulatory breaches and poor management oversight of bank operations.[iii] Customers expect compliance as a pre-requisite and sign of good governance to ensure that banks they are doing business with are not mixed up in criminal activities.

Intense regulatory scrutiny in response to terror funding and other sanctioned transactions has created immense challenges for banks. 20% of financial services have experienced enforcement actions by a regulator, and that number is likely to grow.[ii] Banks face massive fines, operational shutdowns and reputational risk, if they don’t check against regulations and ensure all informational gaps are filled before a transaction occurs. And banks are not the only ones that suffer if they do not comply – their customers are experiencing an impact from the compliance crackdown as well. A bank in Asia was ordered by regulators to completely cease operations due serious regulatory breaches and poor management oversight of bank operations.[iii] Customers expect compliance as a pre-requisite and sign of good governance to ensure that banks they are doing business with are not mixed up in criminal activities.

2. Maintaining a balance of meticulous and rapid screenings is a challenge

Preventing funds from reaching sanctioned politically exposed persons (PEPs) and terrorists is difficult and comes at high operational cost for staff and IT, especially when it must be done without disrupting legitimate transactions. Inefficient screenings with high false positive rates can cripple customer relationships – holding up a large company’s payroll just once due to a false positive with an employee’s name could cause a bank to lose important business. Overly-cautious screen systems can actually flag customers who have the same name as someone on the watch list which might result in loss of customers if these names are treated as fraud.[iv]

Preventing funds from reaching sanctioned politically exposed persons (PEPs) and terrorists is difficult and comes at high operational cost for staff and IT, especially when it must be done without disrupting legitimate transactions. Inefficient screenings with high false positive rates can cripple customer relationships – holding up a large company’s payroll just once due to a false positive with an employee’s name could cause a bank to lose important business. Overly-cautious screen systems can actually flag customers who have the same name as someone on the watch list which might result in loss of customers if these names are treated as fraud.[iv]

3. Updating watch lists is tricky and time-consuming

Today, there are frequent changes to the multiple watch lists that banks need to screen against to ensure they are capturing all sanctioned entities. With growing numbers of sanction lists from numerous national, regional, and global organizations, this step becomes ever-more time-consuming. The number of entities on these lists increases with each update, as do aliases and spelling variations.

Today, there are frequent changes to the multiple watch lists that banks need to screen against to ensure they are capturing all sanctioned entities. With growing numbers of sanction lists from numerous national, regional, and global organizations, this step becomes ever-more time-consuming. The number of entities on these lists increases with each update, as do aliases and spelling variations.

Quality of sanction lists has a direct impact on a filter’s detection capability. As lists become increasingly complicated and intertwined, they require a more sophisticated mix of screening methods and enhancement of the raw data to maintain high quality filtering. A flexible architecture and list handling system is needed to meet current standards and easily adapt to future requirements.

4. Addressing the pain points of transaction screening

Banks need a powerful screening tool in order to avoid illegal transactions, minimize disruptions of legitimate transactions, and keep up with rapidly changing watch lists.

To avoid fines without disrupting the customer experience, compare watch lists quickly while maintaining a low false positive rate. Screening solutions achieve this false positive rate by incorporating historical transaction data and trend analysis. Additionally, effective screens will be able to easily integrate with existing systems makes it so banks don’t have to significantly alter their current IT architecture to implement the solution and keep up with new requests.

Banks have been called on to help stem the flow of money to sanctioned entities. Using a specialized screening solution, such as the Screen solution from Temenos, they can ensure they successfully play their part in catching these transactions. To find out more about Temenos’ Screen solution, visit Microsoft AppSource.

Read more on the Microsoft Banking & Capital Markets and Insurance blogs.

[i] http://www.cnbc.com/2015/10/30/misbehaving-banks-have-now-paid-204b-in-fines.html

[ii] Global Economic Crime Survey, PwC, 2016

[iii] http://www.mas.gov.sg/News-and-Publications/Media-Releases/2016/MAS-directs-BSI-Bank-to-shut-down-in-Singapore.aspx

[iv] https://dealbook.nytimes.com/2014/06/15/bank-account-screening-tool-is-scrutinized-as-excessive/